What a cash flow forecast is and who uses it

A cash flow forecast is a month-by-month view of the money you expect to come in and the money you expect to pay out. The result is a rolling picture of your bank balance through the year, so you can see problems before they arrive rather than after.

Sole traders, freelancers, and small limited companies all use them. They are especially useful if your income is seasonal, if you have large one-off costs coming up, or if customers routinely pay late. A profitable business can still run short of cash if invoices go out before the money comes in and your bills do not wait. The forecast shows you that gap.

Banks and accountants often ask for a cash flow forecast before approving a loan or overdraft. Having a clean, complete one ready makes that conversation much easier.

How the template is structured

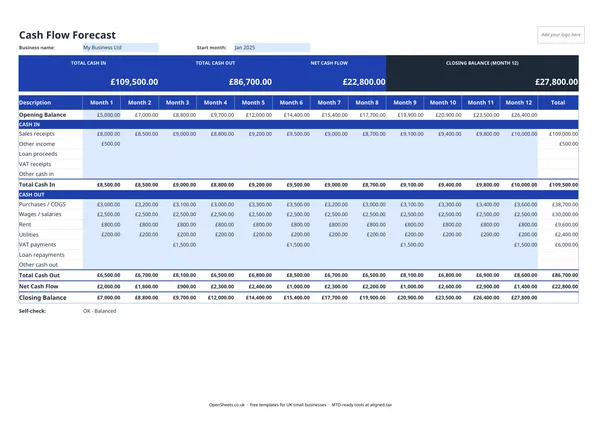

The template covers 12 months, with a column for each month and a Total column at the right. The rows fall into three sections.

Opening Balance. The cash you are starting each month with. You type in Month 1. After that, each month’s opening balance is carried forward from the previous month’s closing balance automatically.

Cash In. Every source of money coming in: sales receipts, other trading income, loan proceeds, VAT receipts if you are VAT-registered, and a catch-all row for anything else. Total Cash In adds these up for you each month.

Cash Out. Every payment going out: purchases and cost of goods sold, wages and salaries, rent, utilities, VAT payments, loan repayments, and any other outgoings. Total Cash Out adds these up for you each month.

The Net Cash Flow row shows whether a given month is cash positive or cash negative. The Closing Balance carries that forward, and the Self-check cell at the bottom confirms the maths balances.

UK-specific points to get right

VAT. If you are VAT-registered, keep VAT receipts and VAT payments separate from your trading figures. The VAT you collect from customers is not your money. It belongs to HMRC. If you fold it into your sales revenue, your forecast will look healthier than it really is right up until the VAT payment date arrives.

Tax payments. UK sole traders pay income tax and National Insurance through Self Assessment, typically in two payments on account (31 January and 31 July) plus a balancing payment in January. These can be large. Make sure they appear in your Cash Out rows for the right months. It is easy to forget them until they land.

Corporation Tax. If you run a limited company, Corporation Tax falls due nine months and one day after your accounting year end. Build it into the forecast for the right month or you will find yourself scrambling.

Seasonal income. Lots of UK small businesses, from holiday lets to garden maintenance to seasonal retail, have income that bunches into certain months. A 12-month forecast makes this visible and lets you plan how to cover the quieter ones.

Common mistakes to avoid

Being too optimistic on the cash in side. Forecasts that assume every customer pays on time, every sale closes, and there are no bad debts are not forecasts. They are wishful thinking. Build in some slack, or run a second version with more cautious numbers.

Forgetting irregular outgoings. Annual insurance renewals, equipment servicing, accountancy fees, and professional subscriptions are easy to miss because they do not show up in ordinary month-to-month spending. Go through your bank statements from last year and look for anything that came up only once or twice.

Confusing profit with cash. You might invoice in Month 3 and not get paid until Month 5. Your P&L books the income in Month 3. Your cash flow only sees it in Month 5. In a business with slow-paying customers, that gap is where things go wrong.

Not keeping the forecast up to date. A forecast is most useful when you replace estimates with actuals each month and look at the updated picture. A static forecast made in January and never touched again tells you very little by June.

Keeping clean records and making MTD easier

Tracking your cash flow each month builds a habit that pays off well beyond planning. The same discipline that has you recording Sales receipts and Purchases / COGS each month is what keeps your bookkeeping tidy through the year.

If your combined income from self-employment and property is over £50,000, Making Tax Digital for Income Tax applies to you from April 2026. The threshold comes down to £30,000 from April 2027 and £20,000 from April 2028. Under MTD you send HMRC a quarterly summary of your income and expenses using MTD-compatible software, rather than filing everything once a year at Self Assessment.

The figures you track in your cash flow forecast are close to what MTD asks for each quarter. If you are already in the habit of recording cash in and cash out each month, the step to quarterly MTD updates is not a big one. Aligned (aligned.tax) is free bridging software that connects your existing spreadsheet records to HMRC’s MTD system and sends the update on your behalf. No new software to learn, no rekeying.