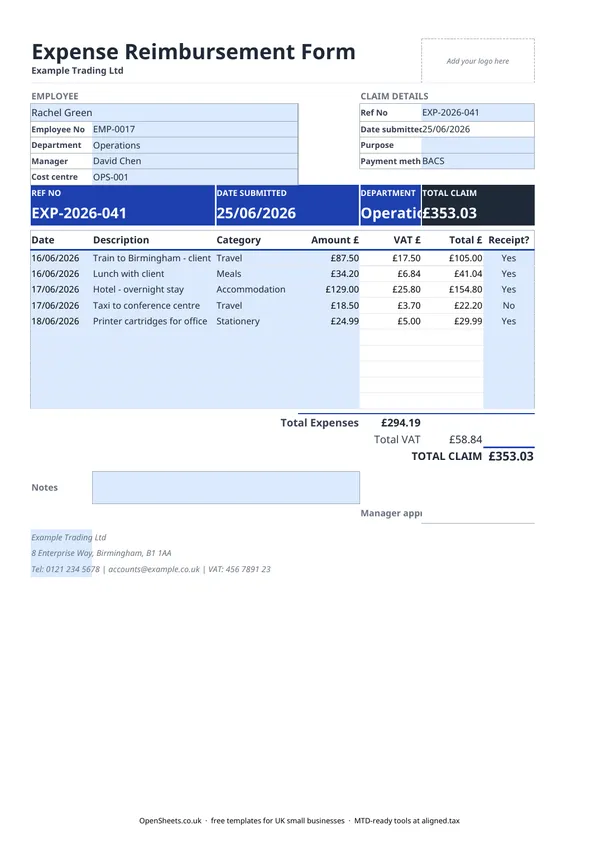

What an expense claim form is for

When an employee or director pays for a business cost out of their own pocket and the company pays them back, there needs to be a record. An expense claim form is that record.

It captures who spent what, on what, when, and why. It is the basis for the reimbursement, the evidence HMRC expects you to hold, and what your accountant or bookkeeper needs to put the cost through correctly.

This template covers the everyday UK business categories: travel, meals and subsistence, accommodation, and stationery. It records the net amount and the VAT separately, so VAT-registered businesses can spot reclaimable input tax at a glance.

Who uses expense claim forms

Expense claims are used by sole traders who employ staff, limited companies with directors and employees, and any business where people spend money on behalf of the organisation before being paid back.

They are also useful for sole traders keeping their own books, as a clean record of out-of-pocket costs that form part of the business accounts.

What HMRC expects you to keep

Business expense records need to be accurate, supported by receipts, and kept for at least six years from the end of the accounting period they relate to.

For most expenses, that means the original receipt or a clear digital copy. The template includes a Receipt column so you can track which items are evidenced. Where no receipt is available, note the reason.

HMRC’s rule is that expenses must be incurred “wholly, exclusively, and necessarily” in the performance of the job. Commuting from home to a regular place of work does not qualify. Travel to a temporary workplace, a client site, or a meeting away from the usual base normally does.

If you are not sure whether a specific cost is allowable, check the HMRC website or ask an accountant. Getting it wrong in either direction costs money: you either miss a legitimate deduction, or you put through something HMRC will push back on.

VAT on employee expenses

If your business is VAT-registered, you can reclaim the VAT on business expenses where you hold a valid VAT receipt. The template keeps net amounts and VAT in separate columns so your finance team or bookkeeper can post the input VAT correctly.

Three things to be aware of:

Business entertainment. VAT on client entertainment (taking customers out for meals, for example) is generally not reclaimable, even with a receipt. Staff-only events are treated differently. Check the HMRC guidance on business entertainment before claiming.

Mixed-use costs. If a meal or journey was partly personal and partly business, only the business portion qualifies.

Fuel. Reclaiming VAT on fuel used for business mileage requires a fuel receipt and a record of business miles. HMRC has detailed rules on fuel scale charges. If this comes up regularly, an accountant can walk you through the right approach.

Mileage rates

Most businesses use HMRC’s Approved Mileage Allowance Payment (AMAP) rates rather than reimbursing actual fuel costs. These are set per mile for cars, motorcycles, and bicycles. Payments up to the approved rate are free of tax and National Insurance for the employee.

The AMAP rates can change at a Budget, so check the current figures on gov.uk before setting your policy. Record the number of miles and the rate in the Description field, and enter the total in the Amount column.

Pay above the AMAP rate and the excess is taxable, reported on the employee’s P11D. Pay below it and employees can claim Mileage Allowance Relief themselves to top up the difference.

Common mistakes to avoid

Missing receipts. A claim without a receipt is hard to defend if HMRC ever asks. Set a clear policy: no receipt, no reimbursement. If that is not practical, require a written note of why the receipt is missing.

Claiming personal costs. The wholly, exclusively, and necessarily test is strict. A meal during an overnight stay on a business trip is different from lunch at the desk on a normal day.

Lumping VAT in with the total. If your bookkeeper receives a combined expense figure without the VAT split, the input tax gets missed. The template keeps the columns separate from the start so this does not happen.

Late submissions. Set a cut-off, one or three months from the date the cost was incurred is common. Late claims make reconciliation messy and can push costs into the wrong accounting period.

No manager sign-off. An unsigned claim is not a complete record. Make sure the approval section is filled in before payment goes out.

Keeping clean records for your accounts and tax

Every approved expense claim is an allowable deduction in your business accounts. Tidy, evidenced records mean your bookkeeper can process them quickly and your accountant can trust the numbers at year end. That saves time and, usually, money.

For sole traders and landlords, clean expense records matter more as Making Tax Digital for Income Tax rolls in. If your combined income from self-employment and property is over £50,000, MTD already applies from April 2026. The threshold drops to £30,000 from April 2027, and to £20,000 from April 2028. Under MTD, you send HMRC a quarterly summary of your income and expenses through MTD-compatible software, rather than one annual return.

The records you keep in a well-organised spreadsheet are exactly what MTD needs. Aligned (aligned.tax) is free bridging software that reads those records and sends the quarterly update to HMRC on your behalf, without moving your data anywhere new. If you are heading toward an MTD threshold, keeping your expense records in a consistent format now makes the transition straightforward when the time comes.