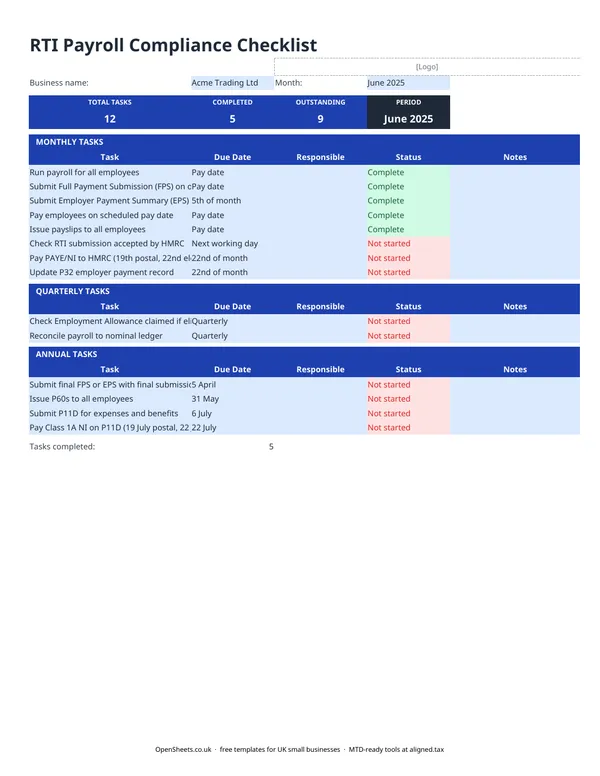

What RTI payroll compliance looks like month to month

Running payroll in the UK is a sequence of deadlines. Miss one and HMRC will notice, because RTI means you are reporting to them in real time, not once a year. This checklist puts all of those deadlines into a single sheet: monthly PAYE submissions and payments, quarterly reconciliations, and the year-end tasks that catch employers out most often.

It is built for small employers, whether you are paying one or two members of staff or running a team of twenty. The tasks, due dates, and status columns mean you can hand the sheet to anyone and it stays useful.

The monthly RTI routine

Every pay period triggers the same short run of tasks.

Run payroll and pay employees. Calculate gross pay, deductions, and net pay. Pay on the scheduled pay date.

Submit the FPS on or before pay day. The Full Payment Submission goes to HMRC on or before you pay your employees, not after. This is the part people most often get wrong. The FPS tells HMRC who you paid, how much, and what you deducted for tax and National Insurance.

Submit an EPS by the 19th if you have anything to adjust. If you are claiming Employment Allowance, recovering statutory maternity or paternity pay, or reporting a period of no payments, the Employer Payment Summary is what you send. It is also what you use for a nil submission if you did not pay anyone that month.

Issue payslips. Every employee is entitled to a payslip on or before their pay date.

Pay HMRC by the 19th or 22nd. The PAYE and National Insurance you have deducted is due to HMRC by the 19th of the following month (postal) or the 22nd (electronic). Check your HMRC online account to confirm the amount due, then tick the task off once payment clears.

Check the submission was accepted. Log into HMRC’s PAYE online service and confirm the FPS was received and accepted. The checklist has a task for this. It only takes a minute and avoids nasty surprises later.

Update your P32. The P32 employer’s payment record is a running total of what you owe HMRC each month. Keeping it updated means your year-end figures reconcile cleanly.

Quarterly and annual tasks

Two tasks fall every quarter rather than monthly.

Employment Allowance. If you are eligible, the allowance reduces your employer National Insurance bill each year. Confirm the claim is set up in your payroll software and that the EPS reflects it. If you are unsure whether you qualify, check the current rules on gov.uk as the eligibility conditions can change.

Payroll to nominal ledger reconciliation. Compare your payroll totals to your bookkeeping records each quarter. Differences that look small in month one turn into headaches by month four.

At year-end (5 April), a further set of tasks comes due. The checklist covers all of them in the Annual Tasks section: the final FPS or EPS with the Final Submission flag ticked, P60s to all employees by 31 May, P11D by 6 July for any benefits in kind, and Class 1A National Insurance by 22 July (electronic) or 19 July (postal).

Common mistakes small employers make

Submitting the FPS after pay day. RTI means the submission must arrive at HMRC on or before the payment date. Submitting the next day is late, even by one day. Set a reminder before the run, not after.

Forgetting the nil EPS. If you did not pay anyone in a month, HMRC still expects to hear from you. A nil EPS tells them no payment is due. Without it, HMRC may estimate a liability and send a notice.

Missing year-end deadlines. The P60 and P11D deadlines come around every year, and the penalties for missing them are real. The annual tasks section of this checklist exists because these are the ones most likely to fall through the gap.

Not reconciling payroll to bookkeeping. Month by month, small discrepancies add up. A quarterly reconciliation catches them while they are still easy to fix.

Assuming Employment Allowance applies automatically. You have to claim it each year via an EPS. It does not carry over. And not every employer qualifies, for example sole directors with no other employees generally cannot claim it. Check gov.uk for the current rules.

Keeping records and digital filing

Good payroll records are good business records. The discipline of running payroll accurately each month, reconciling each quarter, and closing the year cleanly means your payroll costs are properly captured in your accounts too.

If your combined income from self-employment and property is over £50,000, Making Tax Digital for Income Tax already applies to you from April 2026. The threshold drops to £30,000 from April 2027 and to £20,000 from April 2028.

When that time comes, Aligned (aligned.tax) is worth a look. It is free MTD bridging software that connects the records you already keep to HMRC’s MTD system, with no need to move to separate accounting software.